2023年9月6日 星期三

google sheet-appscript-vba-1分K整理

2023年9月5日 星期二

【Python交易程式開發現場59】*產生交易訊號 (17) | 將交易訊號送至下單函數 | 交易訊號下單在OnNotify()

2023年9月4日 星期一

【Python交易程式開發現場41】*產生交易訊號 (4) | 用pyqtgraph畫動態均線圖 (twMASignal.py)

【Python交易程式開發現場20】*畫1分K線(6) | numpy array, tuple的轉換問題 | 時間軸必須為數字的解決 | twCandleStick.py

1. numpy array, tuple的轉換問題

Python中的list与NumPy中array的区别 及相互转换

>>> a=numpy.array([[1,2,3],[4,5,6]])

>>> a

array([[1, 2, 3],

[4, 5, 6]])

>>> tuple(a.reshape(1, -1)[0])

(1, 2, 3, 4, 5, 6)

(1) range(n):表示產生 0 至 n-1 的數列

範例:產生0至10的數列

>>> a=range(11)

>>> type(a)

<class 'range'> #由range函數產生的資料型態為range

>>> a=list(a) #使用list()函數來轉換成串列型態

>>> print(a)

執行結果:[0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10]

(2) range(start,end):start為起始值,end為終止值,產生 start 至 end-1 的數列

範例:產生1至10的數列

>>> a=list(range(1,11))

>>> print(a)

執行結果:[1, 2, 3, 4, 5, 6, 7, 8, 9, 10]

2023年8月4日 星期五

vscode-debug-jupyter notebook

https://pythonviz.com/colab-jupyter/visual-studio-code-jupyter-notebook-integration/

第 4 步:匯出至 Python 檔案或 HTML 檔案

完成 Jupyter Notebook 編程後,自然地我們會有 2 個選擇:

- 把 Jupyter Notebook 匯出成 PDF 或 HTML 檔案,儲存為報告

- 把編程結果匯出成 .py 檔案,讓我們可以使用 Terminal 運作代碼

2023年8月3日 星期四

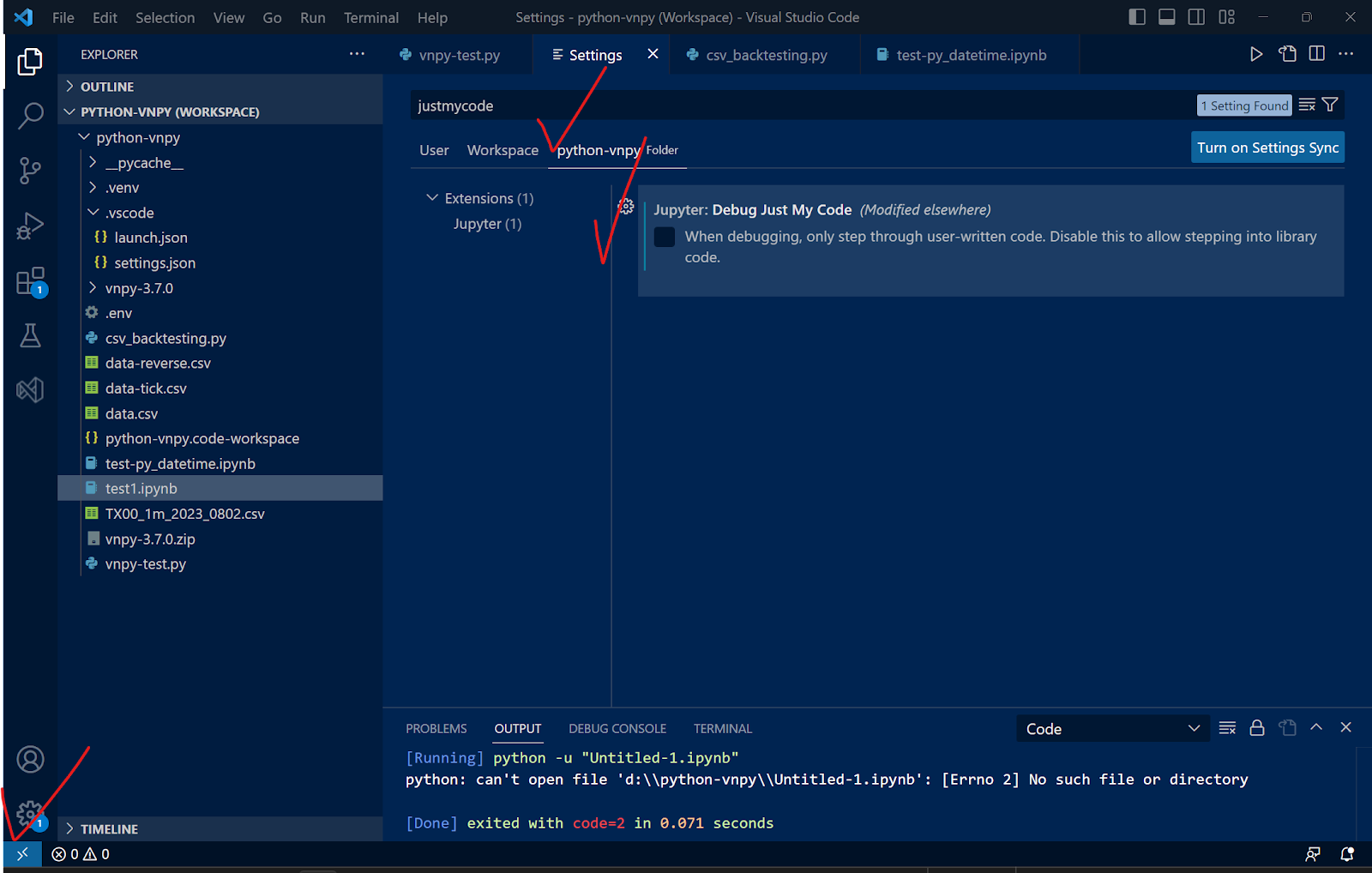

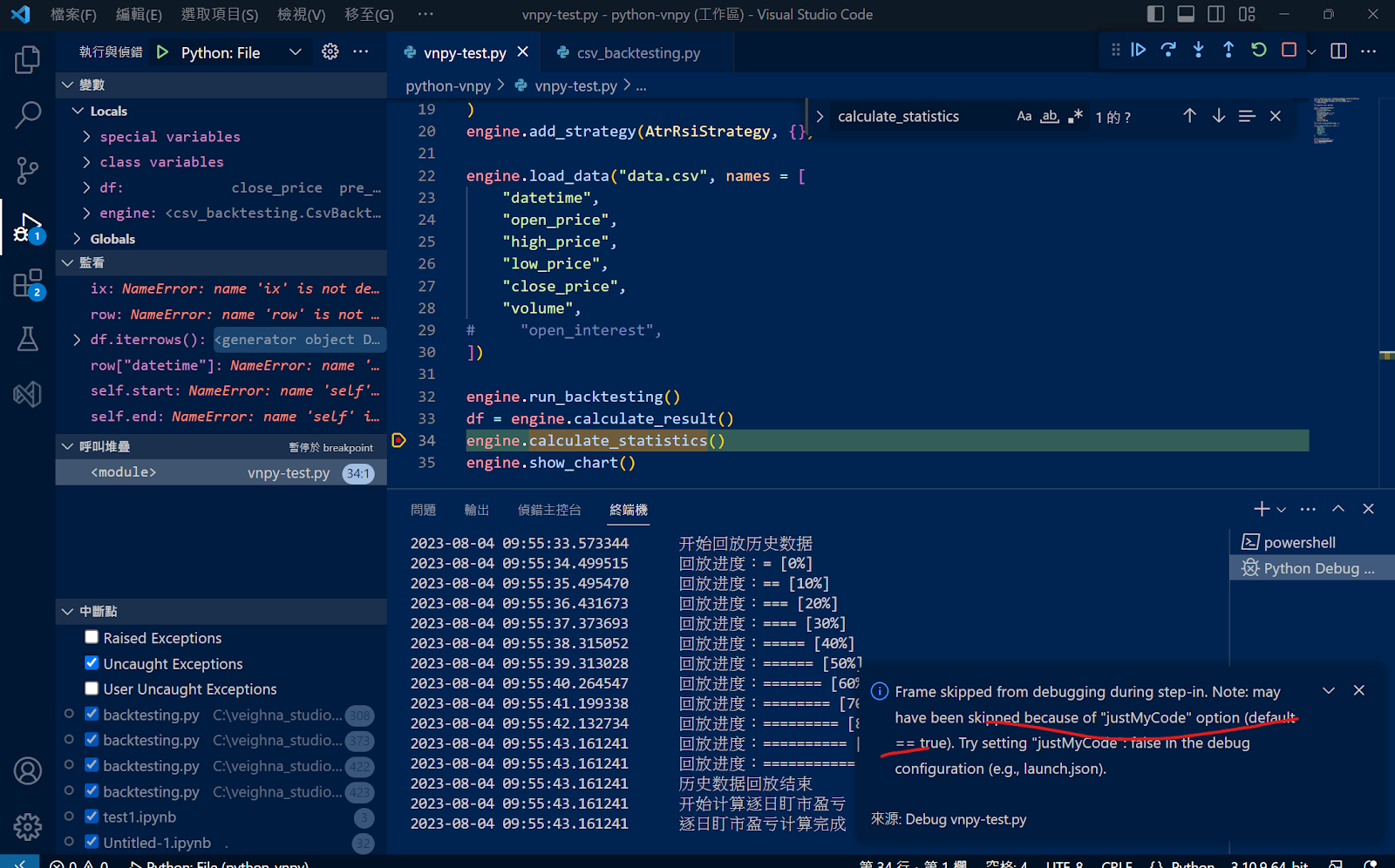

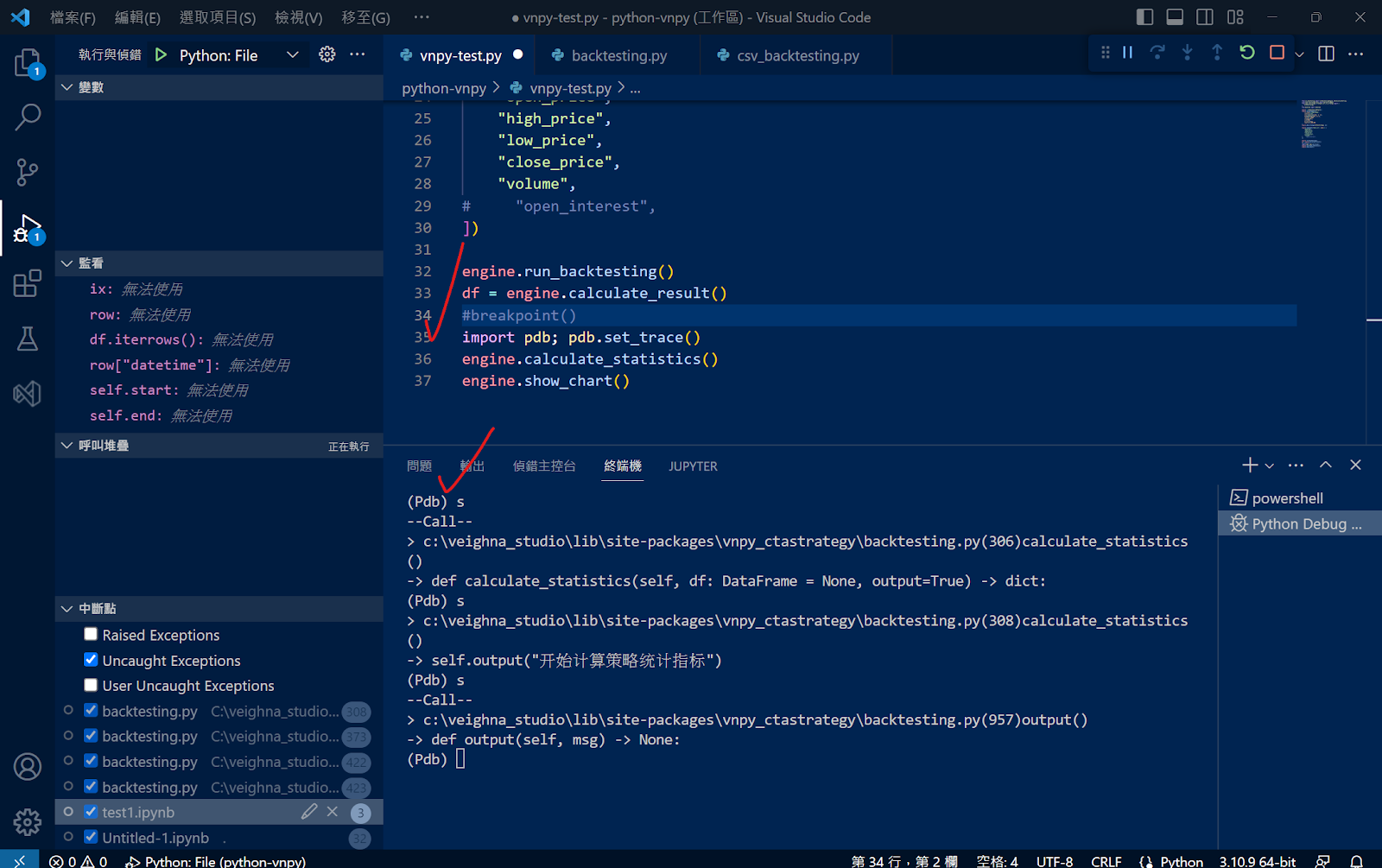

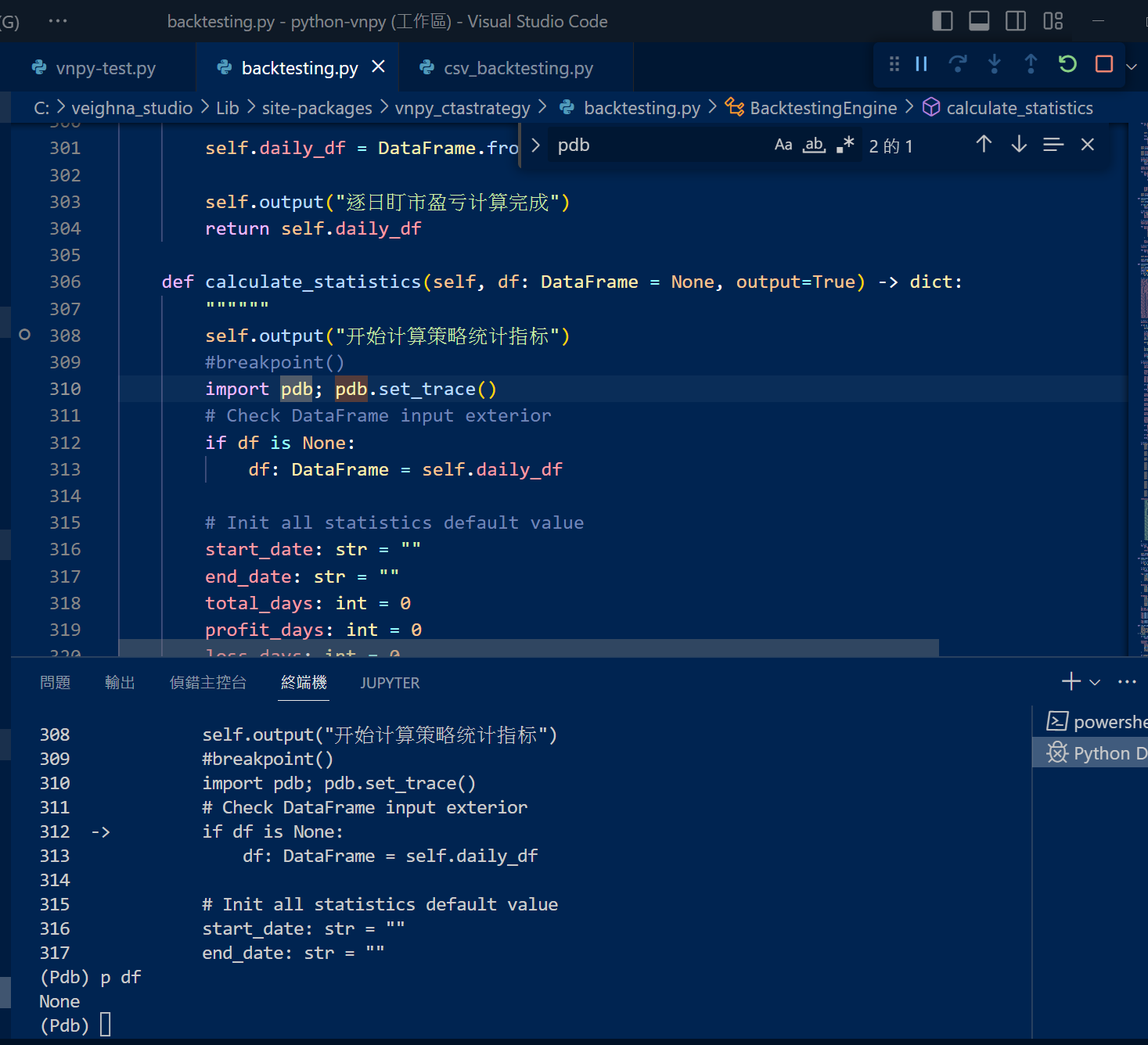

vs-code-debug (pdb能順利trace進入外部程式模組..)(找到了VS Code debug外部程式的關鍵: justmycode=false+purpose: ["debug-in-terminal"])

結論: 最後, 發現真正管用的是PDB..

1. pdb能順利trace進入外部程式模組..

2. pdb.run("print(df)")

3. 還是找到了VS Code debug外部程式的關鍵: 真的是在justmycode=false後面加上purpose: ["debug-in-terminal"]就OK了

4. 不錯的debug功能: 預覽呼叫階層(可以反查某函數被誰呼叫)

[关于vscode调试时跳不到本.py或本.ipynb文件之外的问题_vscode打不开ipynb_Jay E的博客-CSDN博客](https://blog.csdn.net/Edward__J/article/details/129804740?utm_medium=distribute.wap_relevant.none-task-blog-2~default~baidujs_baidulandingword~default-1-129804740-blog-111991099.237&fbclid=IwAR1_J5RbBaO4iZEGaitTVtWXtW1RvtbfFstK2waBugQG8taZZg2m_Smw6pk) [[Obsidian-Highlights]]

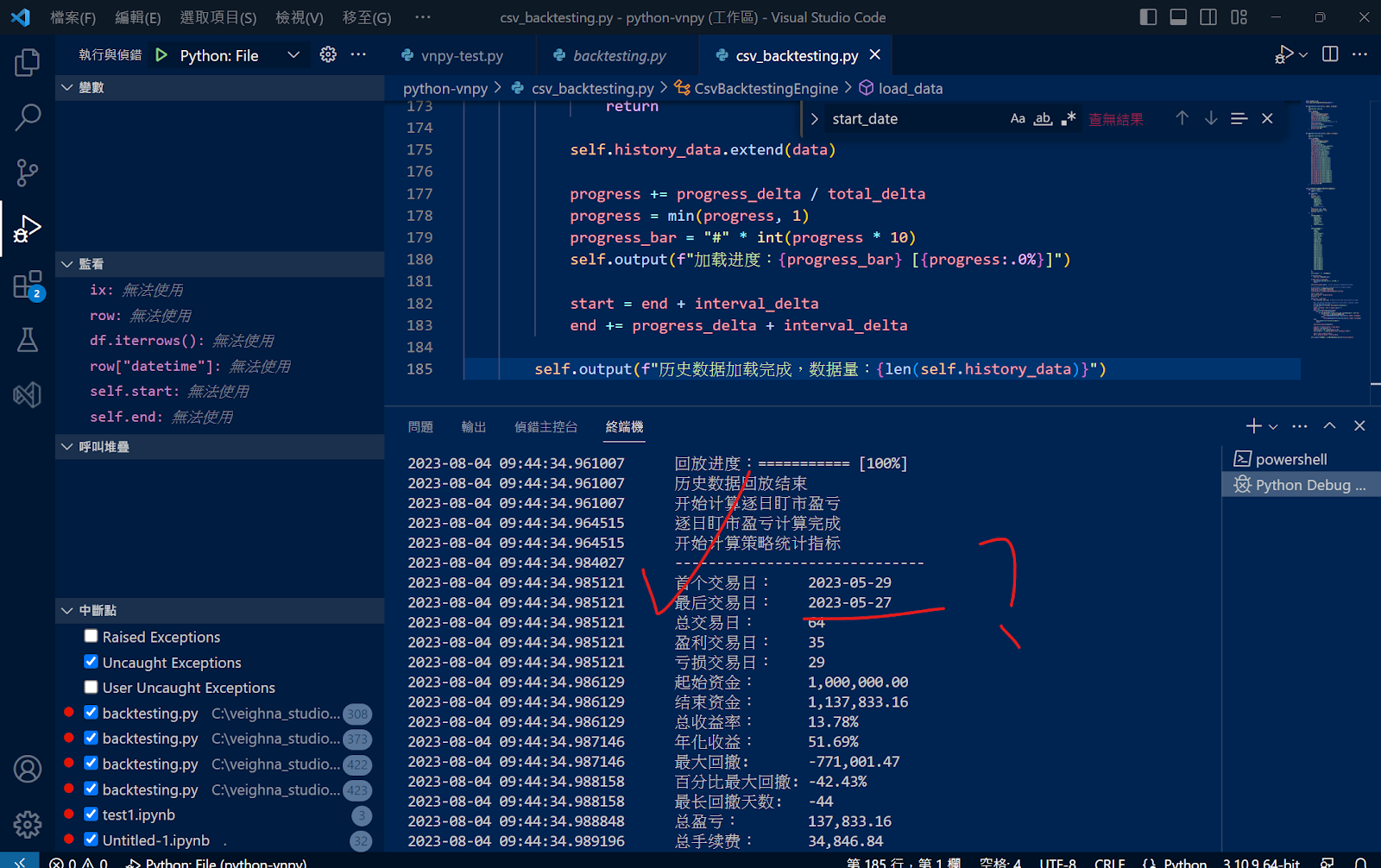

檢查由pd.read_csv所讀入之df, 看來正常..

還是找到了VS Code debug外部程式的關鍵: 真的是在justmycode=false後面加上purpose: ["debug-in-terminal"]就OK了

問題就在以下這段碼產生的backtesting_data有誤:

5. 日内对齐等交易时长K线生成器的实现

5.1 确定K线生成器MyBarGenerator的生成规则

5.1.1 一步到位地解决问题

先给它取个名称,就叫MyBarGenerator吧,它是对BarGenerator的扩展。

不过在构思MyBarGenerator的时候,我发现它其实不应该叫“日内对齐等交易时长K线生成器”。因为我们不应该只局限于日内的n分钟K线生成器,难道vnpy系统就不应该、不能够或者不使用日线以上的K线了吗?我们只能够使用日内K线进行量化交易吗?难道大家都没有过这方面的需求吗?我想答案是否定的。

那好,所幸就设计一个全功能的K线生成器:MyBarGenerator。

为此我们需要扩展Interval的定义,因为Interval是表示K线周期的常量,可是它的格局不够,最大只能到周一级WEEKLY。也就是说您用目前的Interval是没有办法表达月和年这样的周期的。

class Interval(Enum):

"""

Interval of bar data.

"""

MINUTE = "1m"

HOUR = "1h"

DAILY = "d"

WEEKLY = "w"

TICK = "tick"

MONTHLY = "month" # hxxjava add

YEARLY = "year" # hxxjava add顺便在这里吐槽一下BarGenerator:

- 目前的BarData中包含了一个interval字段的,可是它在BarGenerator的时候根本就没有使用过,而使用它本是信手拈来的事情,但是没有却没有使用。如果不信,你可以去看看用它产生出来的bar的内容。

- 另外本来还应该增加一个秒单位(SECONDLY = "1s")的,这个单位其实对高频交易也是很有需求的,可是现在却没有。不知道大家对此有什么看法。

https://www.vnpy.com/forum/topic/30193-che-di-jie-jue-kxian-sheng-cheng-qi-de-wen-ti-yi-ge-ri-nei-dui-qi-deng-jiao-yi-shi-chang-de-kxian-sheng-cheng-qi

-

群益API: m_nCode回報錯誤代碼2017之處理 class MyMainWindow ( QMainWindow , Ui_Form ): def __init__ ( self , parent = None ): super ( ...

-

程式執行時遇到了: ModuleNotFoundError: No module named ‘comtypes.gen.SKCOMLib’ 1. 參考網路解答1:(失敗收場) 問題:ModuleNotFoundError: No module named ‘comtypes.g...

-

終於順利使用 Qt獨特的Model-View架構 . 受不了群益API的python範例檔的設計架構, 用Qt的Model-Views架構重新改寫.. 把核心和介面切割開來, 介面用UI Designer設計完就沒事了, 不用和程式邏輯混在一起.. . 新版的GUI已經慢慢和群益...